This article is part of a longer article sent to Moneyworks Membership Fee client in mid March. We are sharing this again as a reminder, and also for the information of Non Membership Fee clients that receive this newsletter each month.

The one thing that we can say for certain is that currently the outlook is more uncertain than normal. While much of the world is getting back to business after Covid, China and Hong Kong are being locked down and/or are suffering from significant waves of illness from Covid (which impacts the production of ‘things’) and in turn the delay in supply lines you will have been reading about. This may also happen again in other countries.

Inflation is at the highest level in 30-40 years and it is unclear whether it is transitory for the short term, or the long term.

Interest rates are increasing (mortgage interest rates are increasing faster than term deposit interest rates), which affects the returns on both share funds and bond funds.

Who knows what will happen with the Russian War on Ukraine?

Two possible outcomes for Russia/Ukraine proposed by the New York Times are:

A partial Russian Victory: that over the next few weeks a negotiated agreement will be sorted out where Crimea, Donetsk and Luhansk become part of Russia, along with other lands in the South East, providing Russia with a land bridge to Crimea, Ukraine drops it aspiration to join NATO – therefore, a partition of Ukraine.

Putin doubles down: Expanding the fight to Moldova and Georgia, initiate a battle with a NATO country (accidentally or not), using ‘battlefield’ nuclear weapons, or chemical weapons, leading to a drawn out battle with many deaths.

And what will China do? Will they remain ‘apart’ or will they support the Russian military effort, risking sanctions from the West?

However, although we have more uncertainty than a few weeks ago, we do know that for Moneyworks investment and KiwiSaver clients:

- The vast majority of companies that you are invested in are real robust companies that make things or provide services and make strong profits (a couple of ‘innovation companies’ might not be making strong profits just yet).

- That the companies will continue to adapt to ensure that they retain profitability or the track to profitability.

- Your fund managers are working hard (as are we at Moneyworks) to understand what is happening in the world and how that affects your investments. We will let you know if anything needs to be changed based on our understanding of the situation.

- Your portfolios are well diversified and are for the long term.

- Your investments are liquid.

What does this mean for your particular investments?

It is likely that your returns this year will be negative for your portfolio and KiwiSaver – but on the other hand this might be a short sharp correction and we may return to single digit returns quicker. On a positive note, we have seen analysis that show that markets rebound quickly after the cessation of hostilities.

Markets and your share’s related returns have fallen between 5% and 15% since the start of this year.

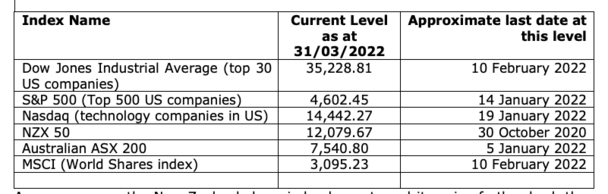

Since the original mid March 2022 communication to Membership Fee clients, markets have come up quite a bit, here are the updated numbers and dates.

To put these falls into perspective the table below this article shows the last date that these indices were at this level.

A. If you have been invested for a number of years

We have been in one of the biggest ‘bull markets’ for many years (over a decade in total), and you will be used to your investments going up on a regular basis. This is a return to normality – that we have been warning about for a number of years – but you probably got sick of us telling you that you might get negative returns – this is it.

B. If you are a new or recent investor

This is part of the investment process, your investments may still be being dollar cost averaged in to the market, in which case, you are purchasing good investments at these lower prices, which is good for your long term investments.

If you have invested in the last year or two, it can be difficult to see your investments not surging ahead, but over time they will gain value.

C. If you have just or are about to retire

This doesn’t make any difference to your investment strategy, unless you were planning to withdraw all your funds and put them in the bank. The plan to take withdrawals from your portfolio will continue as usual and over time your investments will rebound. This is built into the assumptions that we used in developing your retirement savings analysis.

Please contact your adviser or contact@moneyworks.co.nz if you would like to discuss your investment strategy and what is happening, or if you would like to talk to us about your investments and working with us.

Russia

What we do know is that there are many Western companies that have walked away from their operations in Russia (with notifications a few weeks ago, that a law has been signed by Putin to confiscate the hundreds of leased aircraft, so that the Russian airlines can keep flying), meaning that profits for those companies will be impacted. For many companies Russia is a small part of their overall business, so the impact is relatively small.

The war has a direct impact on the supply of oil and gas (leading to the contradictory situation of calls for more coal burning plants to be re-opened, while also calling for more investment into renewable energy). This has seen the prices of these commodities increase, with the West looking for ways to diversify their supply (a big problem for Europe, and Netherlands and Germany in particular.)

Russia and Ukraine are major wheat exporters, and with the sanctions on Russia and the war making life extremely difficult in Ukraine, the supplies of wheat have fallen and the prices have increased. This is going to have a particular impact on poorer countries.

In summary

Volatility and uncertainty is a continual part of investing, and we have had a great run since 2010 with markets giving good returns. It is vital that your investment risk profile reflects your tolerance for risk, and that you are well diversified, both between assets and geographically (as the information on the New Zealand market above illustrates). Investing is a long term project and it is important to understand that there will be ups and downs, it is a normal part of investing.

The important thing is to not make any rash decisions and panic, stick with your long term plan (which your adviser will have developed with you).