KiwiSaver and Australian Superannuation are often compared as if they were two versions of the same idea, but in reality they represent completely different philosophies about how people should prepare for retirement.

One is built on voluntary participation and behavioural nudges; the other is built on compulsion, tax incentives, and scale.

The outcomes reflect those choices — and the differences are far larger than most New Zealanders realise.

Australia’s compulsory system began in 1992, more than 15 years before KiwiSaver existed. Its contribution rate has climbed steadily from 3% to 11% (and soon 12%), meaning every Australian worker receives a substantial employer-funded retirement contribution whether they engage with their fund or not.

This long runway, combined with concessional taxation and strict preservation rules, has created a system with enormous balances:

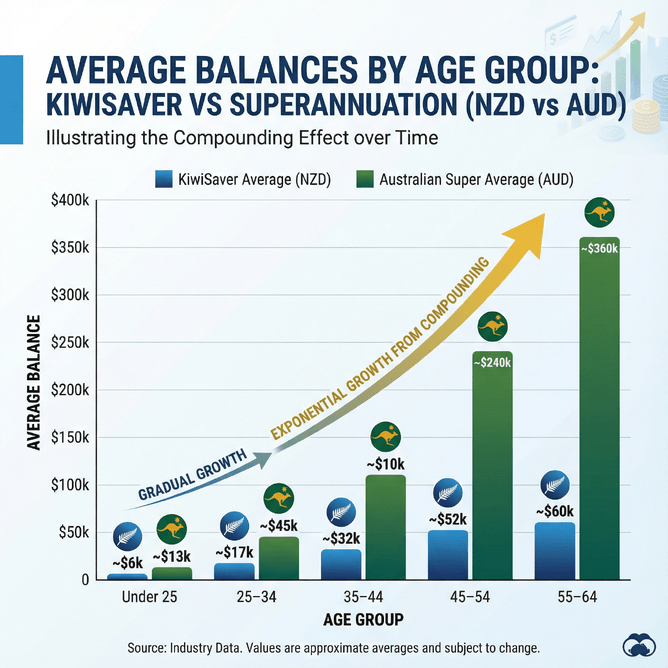

the average 55–64-year-old Australian now holds around AUD $360,000 in superannuation, while the average KiwiSaver member of the same age has around NZD $60,000.

KiwiSaver, introduced in 2007, is a voluntary system designed to encourage saving without forcing it. Most members contribute 3% and receive 3% from their employer, plus the government’s annual top-up. This structure successfully nudges people into saving, but it does not generate the same long-term compounding as Australia’s higher, compulsory contributions.

Tax rules enhance the divergence. Australian super enjoys concessional tax treatment — contributions and earnings are taxed more lightly, and retirement-phase income is often tax-free. KiwiSaver keeps taxation simpler and more neutral, which is fair but does not accelerate balances.

Access rules amplify the difference. Australians cannot withdraw super until preservation age, except in rare cases. This creates behavioural clarity: super is for retirement, full stop. KiwiSaver, by contrast, allows first-home withdrawals and hardship access. These features help people earlier in life, but they reduce long-term balances.

The systems also differ in complexity. Australian funds often include insurance bundles, multiple investment options, salary-sacrifice mechanisms, and navigating the Age Pension means test. These features increase engagement and literacy, especially as balances grow. New Zealand’s system remains intentionally simpler and places far fewer demands on individuals.

Perhaps the most surprising difference is how the systems shape national behaviour.

Australians tend to think about retirement earlier and more often. They compare fund performance, understand contribution strategies, and plan around the pension means test.

New Zealanders rely on the stability of NZ Super and see KiwiSaver as an important supplement rather than the centrepiece of retirement.

Ultimately, the two systems deliver different outcomes because they were designed for different purposes.

KiwiSaver supports people to save more than they otherwise might have; Australian Super ensures they save enough whether they want to or not. Both systems work — but they are not comparable.

Understanding the differences helps New Zealanders set realistic expectations and make better long-term decisions.

We’ve explored this comparison between KiwiSaver and Australian Super in more detail in a short white paper for clients who want to look more closely at how system design shapes outcomes over time.

You can download it here.