KiwiSaver has moved from scrappy teenager to central pillar of New Zealanders’ financial lives.

With nearly 3.3 million members and rapidly growing balances, it is no longer a nice extra. It is a critical part of how people get into homes, survive financial shocks, and fund their retirement.

But as the system reaches adulthood, a set of structural and behavioural problems is starting to show through.

One of the most visible trends is market concentration. Over time, acquisitions, mergers and default-provider decisions have left a handful of large players – mainly banks and a few big independent managers – controlling the majority of KiwiSaver assets.

Competition still exists, but the landscape has shifted from a diverse marketplace to one dominated by scale. This reduces pressure on fees and can tilt industry focus toward gathering funds rather than providing personalised advice.

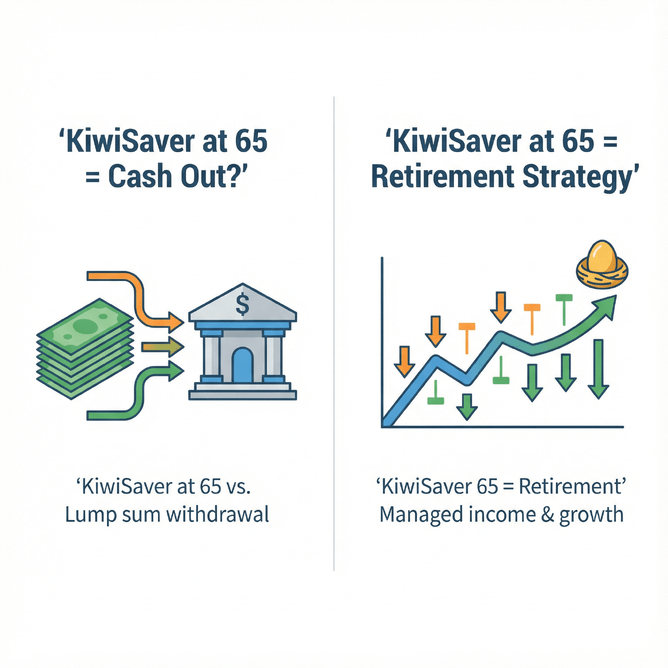

At the same time, member behaviour is not always aligned with long-term outcomes. Many New Zealanders still believe that KiwiSaver should be cashed out at 65, as if access equals instruction. In reality, age 65 is simply the point where retirement planning becomes most important. Yet thousands withdraw into bank accounts, lose investment exposure, and risk running down their savings too quickly.

Others have flocked into aggressive funds after years of strong performance, without fully understanding that these funds can fall sharply in downturns. When volatility returns, we are likely to see a repeat of the COVID-era pattern where people switch to conservative funds at the worst possible time.

Another pressure point is financial hardship. The latest FMA and Inland Revenue data shows hardship withdrawals have surged, both in number and in total dollars. That is not evidence of moral weakness; it is evidence that household budgets are under strain. But each hardship withdrawal erodes balances at precisely the time when compounding should be doing its best work.

Over a working lifetime, repeated withdrawals can be devastating.

The system’s financial architecture also contains subtle drags. Employer contributions are subject to ESCT, meaning that a nominal 3% contribution is significantly reduced after tax. Total remuneration packaging is increasingly common, so the employer’s 3% is often just a reshuffle of the employee’s own pay rather than a true addition.

Meanwhile, fees – including performance fees – remain difficult for many members to understand or compare. The growth of unlisted assets introduces valuation complexity, and ethical branding sometimes outruns the underlying reality of portfolio holdings.

On top of that sits policy instability. Since 2007, KiwiSaver has been repeatedly tweaked: the kick-start removed, the member tax credit reduced, employer tax rules changed, and most recently, the Budget 2025 halving of the government contribution and tightening of eligibility. Each adjustment may be defensible in isolation, but collectively they send a message that the rules can and will change. That undermines trust.

Put together, these issues don’t mean KiwiSaver is failing. They mean the system is being asked to do more than it was originally designed for. A

s a country, we now rely on KiwiSaver for housing, resilience, and retirement. To support that role, contribution rates need to rise over time, total remuneration practices need more transparency, hardship support outside KiwiSaver needs to improve, and fee and ethical disclosure must become clearer.

The system has enormous potential – but it needs a more grown-up framework to match its grown-up responsibilities.

Read more detail by downloading the full white paper from the green button below.