Over the next 15 years, KiwiSaver is likely to become a far more significant pillar of New Zealand's retirement system. Several converging trends, demographic, political, economic and technological, will reshape how people contribute, invest and ultimately draw down their savings.

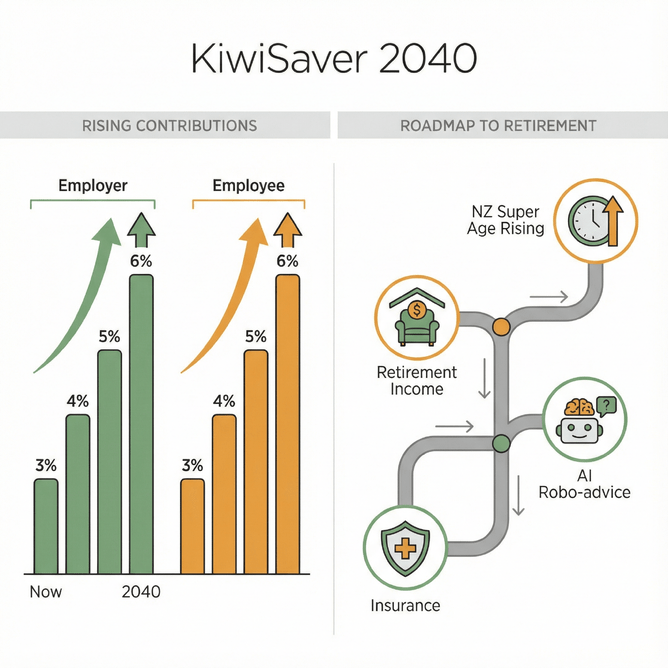

The biggest change already signalled is the proposed gradual rise in default contribution rates, reaching 6% each for employees and employers by 2032. This shift could double the long-term balances of today's younger members. But because KiwiSaver remains voluntary, a new divide will emerge between New Zealanders who increase contributions and those who stay at the minimum 3%. Higher defaults will help many people, but employers will face cost pressures and workers will need better advice on how increased savings affect take-home pay.

Want the full analysis? [Download the white paper]

KiwiSaver for children is another idea gaining traction. A government kickstart at birth, with matched contributions for low and middle-income families, could build an entirely new layer of national savings. Modelling suggests this could create a multibillion-dollar pool by the time those children reach adulthood, improving intergenerational equity and building good saving habits early.

Insurance integration may also grow. Booster already offers life cover and accidental-death benefits exclusively to its KiwiSaver members, similar in principle to Australia's bundled group insurance model. As balances grow, more providers may add protection products, positioning KiwiSaver as a broader financial hub rather than a standalone investment account.

If the NZ Super eligibility age eventually rises, KiwiSaver's withdrawal age will likely rise in parallel. This would require better bridge-planning and structured decumulation products. New Zealand is well behind international peers here; most countries provide default withdrawal pathways or lifetime income products. The success of Lifetime Retirement Income hints at what a KiwiSaver-linked decumulation ecosystem could one day look like.

Technology will transform the member experience. Robo-advice is already permitted, but the next decade will bring AI-driven KiwiSaver coaching that interprets pay rises, spending patterns and life events to prompt contribution changes or fund adjustments. The regulatory challenge will be drawing boundaries between information, advice and persuasive design.

Further ahead, KiwiSaver may see changes to tax treatment, first-home withdrawal rules, climate and ethical regulations, auto-enrolment, auto-escalation of contributions, and provider consolidation. These forces could shift KiwiSaver from a voluntary nudge system into a semi-compulsory retirement engine that supports national infrastructure investment, shapes corporate governance, and reduces long-term pressure on NZ Super.

For members, the decisions made now, contribution levels, fund choice, ethical preferences and long-term planning, will matter more than ever as the system matures into its next form.

For a more detailed analysis, download our white paper below.