Over the years, we have set up quite a lot of diversified investment accounts for our clients for their children and grandchildren.

Time is a powerful ally of the investor – with us seeing more and more Grandparents keen to invest on behalf of their Grandchildren. As we know investing money for a child’s future can last well beyond birthdays and Christmases.

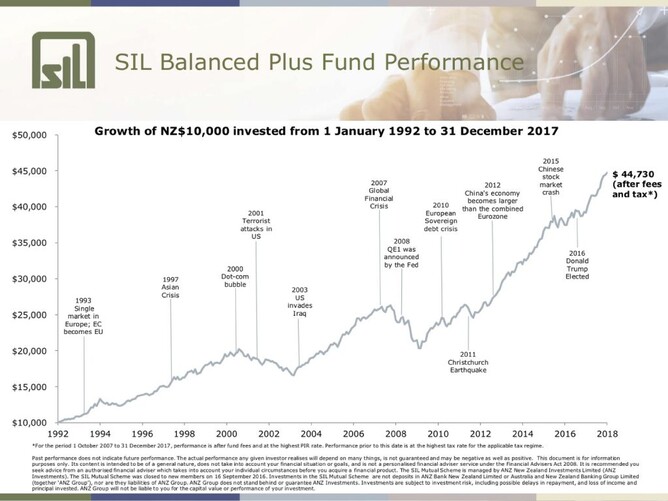

How does time work? The best example is this graph of $10,000 invested since 1January 1992 until the end of 2017 - as you can see, even though there are dips, as long as the time period is long enough, a diversified balanced fund will do its work and grow.

We are organising accounts for our clients every week or two now, but it is important for you to know that our preferred provider for these accounts (ANZ) are unfortunately unable to open an investment in a child’s name and have Grandparents as authorised signatories.

The authorised signatories will need to be the child’s parents or legal guardian.

So what options do Grandparents have?

There are two options for Grandparents (or other non-legal guardians) to open an investment account for a child.

These are:

Option one

Open an investment in the child’s name with their parents as authorised signatories:

- This means the account will be in the child’s name

- The PIR Tax rate is the child’s

- A certified birth certificate for the child will be required

- Parents or the legal guardians will manage the funds until the child reaches 18 years old at which point the fund will revert to the child

- The account will be addressed to the child’s parents address, not Grandparents, and

- The Grandparent/non-legal guardian will have no access to view or monitor the account information.

Option two

Open the investment in the Grandparents name:

- This will mean all accounts will be in the name of the Grandparent

- The PIR Tax rate will be the Grandparents

- Only the Grandparent will have access to view and monitor the fund details

- All account information will be addressed to and sent to the Grandparent

- When the child reaches 18 years of age (or at any age over 18) the Grandparent can transfer the investment to the child’s name.

It is important to note that for either of the above options all parties will need to provide full identification.

If this is something that you are interested in, get in touch with your adviser and we will work through this with you at contact@moneyworks.co.nz