Please note that the table above was to the end of April (the markets have since rebounded higher)

For a long time (from the fall of the Berlin Wall until recently) the world was in a historically stable period. But in the last five years and in the last six months in particular, we have seen significant change in the world.

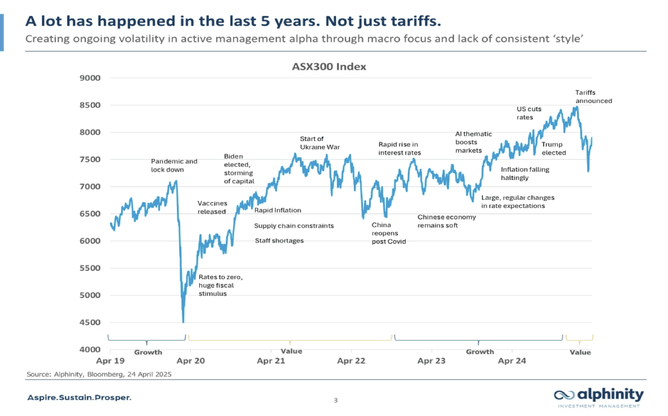

The graph above is from an excellent webinar run by one of our fund managers - Alphinity. We use the Alphinity Sustainable Share Fund in our clients portfolio's - which invests in the ASX300 index (the large companies index in Australia). But the pattern is the same if you look at most other indices over this time period.

A number of commentators consider that we have had a 'golden period' from the fall of the Berlin Wall until Covid (2020), but the global situation may have started breaking down earlier - possibly from the Global Financial Crisis in 2008 - 2011.

The 'golden period' saw globalisation, peace around the world (ie limited to no inter country wars), continual growth in Global Domestic Product (GDP), standards of living lifting around the world, poverty reducing and many other factors and indicators improving.

Although the last six months have seen uncertainty and turmoil which is unprecedented in our lifetimes, there has been uncertainty for longer (just not at the whim of one person and changing from hour to hour or day to day).

If we focus on the last five years - since Covid turned the world upside down and created supply chain issues, the graph above shows the many factors that have impacted on investment markets.

We need to focus on the new normal.

Wars between countries that appear to be unstoppable and unsolvable (Russia/Ukraine and Israel/Gaza).

Unpredictability of President Trumps mood and therefore impact on tariffs and the USA's treatment and relationship with other countries.

Destruction of the global soft power of the USA - and China stepping confidently into voids.

Significant loss of funding for the traditional world leading research in the US in the scientific, health and other industries.

Inflation (nascent for decades) now being a real factor to consider.

Attractive investments are changing.

More fund managers are focussing on 'defensive' stocks - investments that have a continual income despite the economic cycle and conditions (eg infrastructure regulated by government, consumer staples) instead of cyclical stocks that flourish when there is economic growth and certainty.

More expenditure globally on defence (including New Zealand), providing opportunities for investment in industries that support these industries - not necessarily companies making weapons or weapons components. Think uniforms, Information Technology, Cybersecurity, electronics, advanced manufacturing, communication services.

More diversification away from US based companies. One of the best performers in recent times in our portfolio's has an investment strategy strongly focussed on Asian equities.

With the uncertainty relating to tariffs and changing rules in the US - it is possible that many companies will continue to invest in their businesses, because they don't know when the rules will change next.

The investment environment is changing rapidly (daily) and it is important that you have the right investment managers, who can adapt to the changes. This is why Moneyworks recommends mainly 'active' investment managers, where the investment decisions are made by human brains, not by computers or set and forget index tracking funds.

What can you do?

Remember you are investing for the long term. If you are investing for the short term (ie less than five years), your investments should probably just stay in the bank - unless you fancy yourself as a day trader - Sharesies can help you with that if that is your goal.

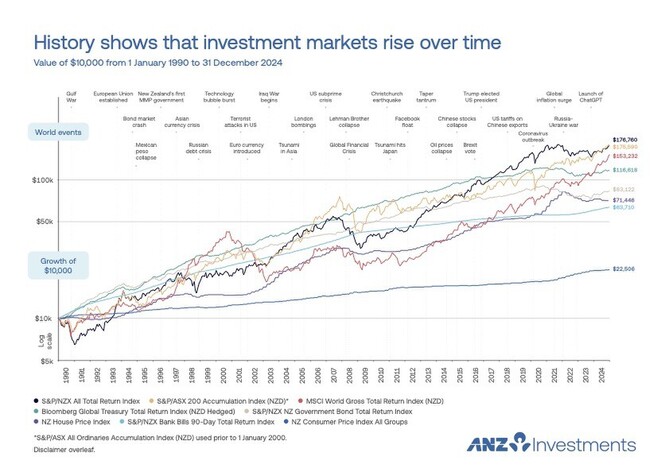

Referring to the diagram above, over the long term share values increase. If your investments are held in a long term strategy, your fund manager won't be taking bets on short term gains.

Make sure that you have a good reliable investment manager(s) working for you, that will work hard for you to understand the world and events when investing your money.

Make sure that your financial adviser is one that you are comfortable with, that you can ask questions of, that keeps you up to date with education and information.

In times of such volatility and uncertainty, we strongly recommend that the bulk of your investments are held in 'active' funds, where they can quickly adjust to the changes in the world.

The graph below shows more perspective, with information on markets for 34 years from 1 January 1990 until 31 December 2024

At Moneyworks we continually research and evaluate the fund managers that we recommend to make sure that they are doing what they say they are doing. We also work hard to get a range of fund managers who work in different ways, that see the world in different ways (but none yet have a crystal ball).

Finally, if you are unsure, talk to your financial adviser, that is what we are here for, to help you understand.