My morning newsletter from The Economist is a valuable part of my day - even when I am too busy to read all the other newsletters, I save the Economist newsletters to check when I have time.

The newsletter has between 3 and 5 summaries of articles, and you can get a limited free subscription. Often the summary gives enough detail to understand what is happening, but sometimes, the information in the summary or the picture is just too enticing, and I have to pursue the information. For your own subscription to the daily newsletter, click here.

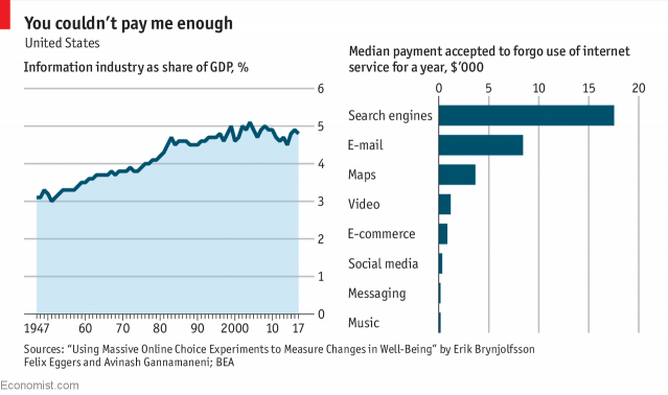

One that took my fancy recently was this graph

Thanks to The Economist for this commentary as well:

ONE of the great riddles about the American economy is why its growth has slowed down so much during the past few decades. Between 1946 and 1975, America’s GDP per person grew at an average annual rate of 2.3% a year. On average, it has grown by just 1.8% a year since.

Many economists believe that national accounts may underestimate the economic significance of technological innovations. Despite the advent of the internet, smartphones and artificial intelligence, the official value added by the information industry as a share of GDP has scarcely changed since 2000. What might explain this paradox?

Part of the problem is that GDP as a measure only takes into account goods and services that people pay money for. Internet firms like Google and Facebook do not charge consumers for access, which means that national-income statistics will underestimate how much consumers have benefitted from their rise.

One way to quantify how much these internet services are worth is by asking people how much money they would have to be paid to forgo using them for a year. A new working paper by Erik Brynjolfsson, Felix Eggers and Avinash Gannamaneni, three economists, does exactly this and finds that the value for consumers of some internet services can be substantial. Survey respondents said that they would have to be paid $3,600 to give up internet maps for a year, and $8,400 to give up e-mail. Search engines appear to be especially valuable: consumers surveyed said that they would have to be paid $17,500 to forgo their use for a year.