It is time in the market - NOT timing the market - the role of FInology in investing

It is tempting to stop making regular investments into markets when there is volatility and you hear the media pronouncing that the markets have 'crashed', 'plummeted', 'plunged', or even when they breathlessly talk about the markets falling - the biggest fall in 10 years.

As financial planners, we do many things that are valuable to our clients, develop a retirement savings analysis so that our clients can see how long their money will last in retirement, make sure that they have well diversified and liquid investment portfolios, and ensure that their insurances are going to work for them, and are the appropriate ones for them.

But the most value that we add is in the 'finology' part of our work. This is the Financial Psychology aspect of our work, and when markets are volatile and falling, the most important thing we can do is to remind our clients to keep with the plan.

The normal human reaction tends to be a variation on:

a. 'what can I do, this doesn't feel good', '

b. 'why don't I stop adding money to my investments',

c. 'should I pull all my money out of my risky investments?'

d. 'Is this the time to change my risk profile to be more conservative?'

It is hard to understand (unless you have been here before), that now is actually the time NOT to change any of your behaviour. Withdrawing your money will lock in those temporary losses and turn them into permanent losses, changing your risk profile to be more conservative can have the same effect.

This is why we talk regularly with our clients that wish to engage with us - in particular our Membership Clients that we meet with every year, to make sure that their risk profiles are appropriate, that they understand the theory and information behind staying put, that markets rebound and that:

If you are making regular investments into your KiwiSaver or investments, this is the time when your fund manager will be buying you good investments at cheaper prices. Remember, just before the market fell, people thought those investments were worth more than they cost today. At Moneyworks, our job is to ensure that our clients have fund managers that are good at doing their job and are buying good quality companies for our clients to invest in.

It is also our job to keep you on course, despite your emotions, and natural 'fleeing' instincts. That is our job, which is why we are sharing this information with you, to remind you of this information.

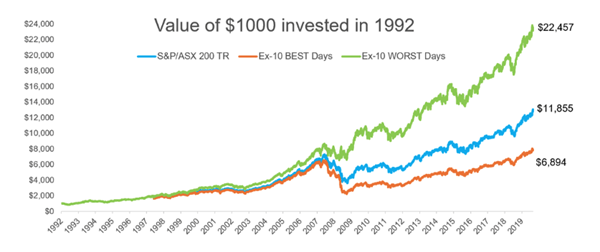

The graph above is insightful. It shows the Australian S&P/ASX 200 index - the top 200 companies listed on the Australian share market. This chart is just one example of what it is illustrating, the diagram can be found for all major markets internationally.

The BLUE line shows the change in $1,000 since 1992, at the end of 2019 that amount would have grown to around $11,855.

But it is the other lines that are very insightful.

The GREEN line shows that you would have almost doubled your money by avoiding the 10 WORST days in the market. So theoretically, you would have been best to get your crystal ball out and taken all of your money out of the market before those days, and then put your money back in straight away. BUT - how are you going to know when that worst performing day is? We can only know that information in hindsight.

The ORANGE line then shows something even more interesting, if you had made a mistake and taken your money out in anticipation of the worst days, but ended up missing the 10 BEST days of investment, you would have had a total value of almost half that of the Green line. That is, if you had left your money invested, through good and bad days.

As the creator of this chart notes:

"To make matters even more challenging, the biggest daily gains in the equity market are closely followed (or preceded) by the biggest daily losses. Large gains and losses tend to cluster. With the largest gains/losses in the past three decades clustering around the Asian Crisis/tech stumble, the GFC, The EU Sovereign Debt Crisis and during concerns around slowing China/Global growth. The increased volatility during these periods increases risk to the upside and the downside."

Patrick Hodgens - the creator goes on further with an interesting case study in market timing which we have shared below:

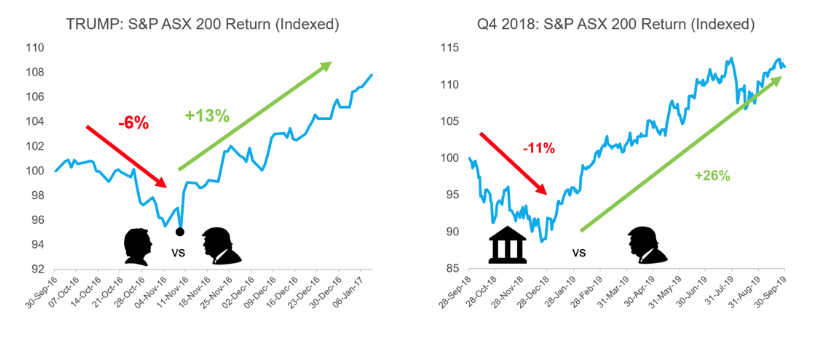

Trumped’ timing: A case study in market timing

In August 2016, I reached out to 30 different professional investors, CEO’s and market experts to ask them two simple questions:

- Can Donald Trump win the US election?

- If he does win, what will the subsequent direction of the share market be?

80% of respondents told me that Hilary Clinton would win the 2016 election. It seems obvious with hindsight that wasn’t going to be the case. But at the time, this view was consistent with polling and betting markets which gave Clinton a 5 to 1 probability of becoming the next US President.

The answer to the second question was even further from the truth. 95% of respondents said that if Trump did win, equity markets would fall by 10% (on average). As the probability of Trump winning increased in the lead up to the election, equity markets started to fall.

The first chart below highlights what happened when Trump was announced as US president in November 2016. Some of the most successful CEO’s and investors in the country got not only the result wrong, but the direction of the share market wrong too.

More recently in Q4 2018, inflation had reared its head and the risks of global trade wars escalated further. The market reacted swiftly, selling off global and Australian shares which fell over 10% during the quarter.

However, on the back of no new news, the market direction changed on 23 December 2018.

Urged on by a pivot in the US Fed policy toward an easing bias, the market subsequently increased by over 26% in the next 9 months – and has continued to rise to new heights today. As the second chart below shows, investors who moved into cash, had to move back into equities swiftly in order to capture the subsequent gains.