2022 will go down as one of those years that investors will talk about forever. Not only did the share markets fall around the world, but bonds (or fixed interest) fell as well.

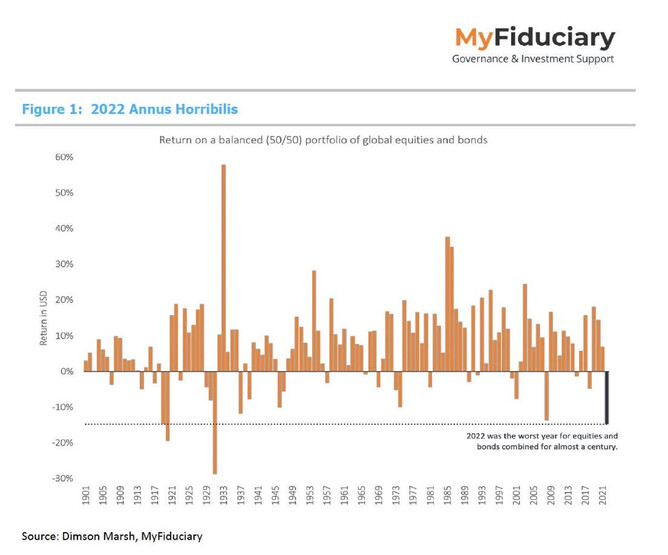

The graph above shows the impact of this unusual dual fall on a balanced portfolio (this graph assumes that a balanced portfolio is 50% growth – equities and property, and 50% fixed interest and cash).

If you are feeling rattled by the investment returns and values, it is because between the two asset classes falling, 2022 was the worst year for equities and bonds combined for almost 100 years. The last time this happened (and things were worse) was around the 1929 crash and when you check out the graph, you will see that most times that returns were this unpleasant the markets rebound strongly within a few years.

Building a portfolio, the goal is to have different asset classes so that they act differently at different times, to protect a portfolio. This has worked historically, but not in 2022. As interest rates increased over the year, listed property and infrastructure (which usually protect in a portfolio) also saw some lower returns.

All in all a perfect storm (oh and of course we had Putin invading Ukraine, the supply chain and labour issues as a result of Covid and of course climate change impacts). One heck of a year!

But looking back at the table above you see how things rebound.

A few things to note now:

1. Term Deposit rates are looking good – over 5% with mainstream financial institutions, we have been using these in our clients portfolios for some time now.

2. Every major bull market has been proceeded by a bear market (and the bigger the bear market, the bigger the subsequent rebound) (This information is from Fisher Funds Ashley Gardyne in Business Desk).

“Following a fall of more than 25% in the US benchmark S&P 500 Index, there have been significant positive returns in the following year in most cases, he said. “And, on a three-to-five-year view, returns have always been positive, often materially so.”

Gardyne’s number crunching of the seven times since 1961 that the S&P 500 had fallen more than 25% showed the average rebound the following year was 17%. The average return over the following three years had been 37% and after five years, 83%, while returns averaged 214% after 10 years. However, the depths of each bear market varied greatly from the 27% decline between 1980 and 1982 to the 49% decline in 2000 to 2002, and the 57% decline in the 2007 to 2009 global financial crisis (GFC).

3. While the markets in the 2007 – 2009 period took longer to recover, they still bounced back up and went on to provide the 10+ year bull market that we have just seen in equities.

4. The companies that led the last bull market are not likely to lead the next bull market – which is what your fund managers are spending a lot of time working on – working out which companies are going to lead in the future.

The keys to having a long term successful portfolio and investment strategy are:

1. Have great quality companies and investments (and not investments made of air)

2. Have a well diversified investment strategy

3. Manage your cash flow so that the funds that you need to access are readily available for up to a couple of years, so that you don’t have to cash in investments when they are down.

4. Work with advisers and investment managers who have experience, skills and robust processes to take advantage of the different market conditions.